Just a heads up for a new PFS Buyers Club coin deal in case you want to get in on over $5,000 in spending. Tomorrow, March 17, the US Mint is releasing a new set of coins at exactly 12pm ET. The coins will cost ~$5,337 and all cards except US Bank/Elan (Fidelity) cards should work to earn miles, points, or cashback.

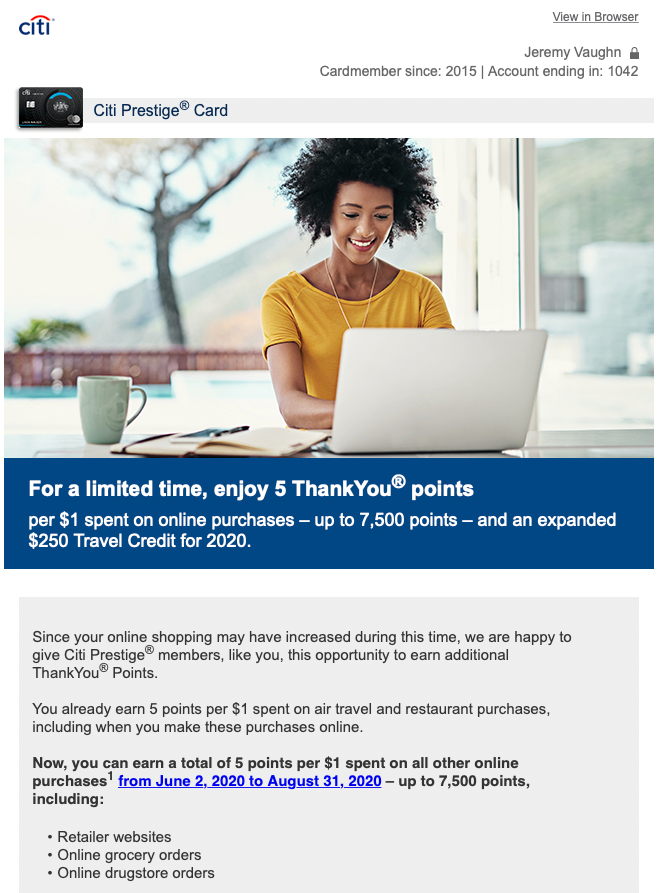

There’s some speculation that Amex cards *might* charge a cash advance fee. Incidentally, I just got the Amex Gold card in the mail yesterday and need to meet the minimum spending requirement. But I think I’ll use my BofA Premium Rewards card for 2.62% cashback (~$140) instead.

Here are the coins that go on sale tomorrow

Aside from minimum spending, you could also gain traction toward spend bonuses like free hotel nights (Hyatt, Hilton), elite status (AA cards), or any other promotions you’ve signed up for.